When you purchase through links on our site, we may earn a commission at no extra cost to you. Learn more.

Your dog starts limping out of nowhere. You get it checked out, and then the alarming estimate comes back — it’s in the thousands.

Table of Contents

This is when a lot of people think: “It’s okay. We’ve been saving for this.” The problem? Your account only has a few hundred dollars in it.

Let’s be real — that’s the part no one talks about. The “just save $50 a month” plan sounds smart. But when you actually line it up against real vet bills, the math gets uncomfortable pretty quickly.

The Common Advice (Why It Feels Smart)

You’ve probably heard this before: “Just skip pet insurance and put $50 a month into a savings account instead.”

At first glance, it sounds like a smart, no-nonsense plan.

You’re setting money aside consistently, you know exactly where it’s going, and you’re not dealing with policies, reimbursements, or fine print.

Why Savings Appeals To People

A major part of the appeal is control.

- You decide how the money is used

- You can access it anytime

- If your dog stays healthy, nothing feels wasted

And if it’s sitting in a savings account, it might earn a little interest over time (though not much).

None of that is wrong. Saving for your dog is a responsible move, and it works well for smaller, expected expenses.

But this is where the plan starts to get tested. Not because the idea is flawed, but because it often doesn’t align with how veterinary costs actually look.

That’s where the gap starts to show.

The Math Problem

Let’s actually run the numbers, because this is where the “just save a little each month” plan starts to feel different than it does in theory.

If you’re setting aside $50 a month, that’s $600 a year. Over time, that builds very gradually:

- After 1 year: $600

- After 2 years: $1,200

- After 3 years: $1,800

- After 5 years: $3,000

- After 8 years: $4,800

That’s steady progress. But the timeline matters more than the total.

What Major Vet Bills Actually Look Like

Here are a few common (and expensive) scenarios:

- Emergency visit with diagnostics: $1,500–$3,000

- Intestinal blockage surgery: $3,000–$6,000+

- Cranial cruciate ligament (CCL) tear surgery: $4,000–$6,500+

- Cancer treatment: $5,000–$10,000+

It doesn’t take multiple emergencies for this to become a dire financial issue. One serious incident is enough.

Where The Math Breaks Down

Let’s use a straightforward example.

If your dog needs a $5,000 surgery, it takes about 8 years of saving $50/month to get there.

That’s the part most people don’t stop to calculate. The monthly amount feels manageable, so the timeline gets overlooked.

“I’ll Just Save More”

This is the natural next thought, and it helps, but not as much as people expect.

- $100/month → $1,200/year

- $200/month → $2,400/year

Now look at how that lines up early on:

At $200/month:

- 3 months: ~$600

- 6 months: ~$1,200

- 1 year: ~$2,400

That’s a meaningful jump, but it still doesn’t cover most major procedures, especially early on.

The Core Issue

Saving more speeds up the timeline, but it doesn’t change the structure.

You’re still building toward a number over time, while the kinds of expenses you’re preparing for can happen long before you get there.

The Timing Problem: Dogs Don’t Wait

The math is one thing, but real life doesn’t follow a timeline.

Most people don’t start saving with a specific deadline in mind. The assumption is simple: by the time something serious happens, there will be enough set aside.

Sometimes that’s true, but often, it isn’t.

Why Timing Works Against You

Dogs tend to run into problems early and not always in predictable ways.

- Puppies chew things they shouldn’t

- Young, active dogs push their limits

- Even routine play can turn into an injury

And many of the most expensive issues, like torn ligaments, swallowed objects, or sudden illness, don’t build up over time. They hit fast, with little (or no) warning.

Where Savings Plans Get Tested

This is where things start to break down. Saving happens in small, predictable increments over time.

Vet bills don’t follow that pattern. They tend to show up:

- All at once

- Without any warning

- With a high cost that needs to be paid immediately

That mismatch is what creates the problem.

Because in that moment, you’re not working with what you planned to have — you’re working with whatever is actually there.

Did You Know?

Many of the most expensive vet emergencies, like swallowed objects or ligament injuries, happen in young, otherwise healthy dogs, not older ones. Translation: the highest costs often show up before your savings have time to catch up.

What If A Health Problem Happens Early?

Saving $50 a month works — eventually.

The question is whether you have enough when it actually matters because most vet emergencies don’t happen on your timeline.

So let’s break down what this looks like in practice.

It Starts Earlier Than You Think (Month 3)

You’ve been consistent and set aside about $150 so far. Then, your dog swallows something they shouldn’t.

What starts as a quick visit turns into imaging… monitoring… possibly surgery.

- Estimated cost: $2,500–$4,000+

That’s not some rare worst-case scenario. It’s one of the most common reasons dogs end up at the emergency vet.

At this point, your savings account helps, but only a little. The rest of that bill has to come from somewhere else.

Would you feel comfortable covering that gap?

Just When It Feels Like You’re Getting Ahead (Year 1)

Now, you’ve got about $600 saved. That’s a solid start.

But now imagine your dog tears a ligament chasing a ball or jumping off the couch.

- Estimated cost: $4,000–$6,000+

You didn’t do anything wrong here. You planned ahead. You’ve been consistent. But the numbers still don’t line up.

How much of that bill can you actually cover?

Still Not There Yet (Year 2)

Now you’re sitting at around $1,200. At this point, the savings can definitely help with smaller issues.

But let’s say something more serious comes up — an intestinal blockage, a sudden illness, or a surgery that can’t wait.

- Estimated cost: $3,000–$6,000+

Now you’re covering a bigger portion, but you’re still not all the way there.

What This Shows

The issue isn’t saving. It’s where you are when something happens.

There’s a stretch of time, especially in the early years, where you’re doing everything right, but you’re still not fully covered yet.

And that’s the gap most people don’t think about until they’re in it.

That’s also before you factor in something else most people don’t think about — how often that savings ends up getting used for things that have nothing to do with your dog.

Have you ever had something like this happen with your dog?

Let’s Be Honest: A Savings Account Doesn’t Stay Untouched

In theory, that savings account is there for your dog. In real life, money rarely stays perfectly assigned to one purpose.

Life happens. A car repair. A home expense you didn’t plan for. A trip that costs more than expected. Something always seems to pull from that “just in case” fund.

And because it’s your money — and easy to access — it’s hard not to use it when something else feels more urgent. That’s the tradeoff people don’t really talk about.

Flexibility is the benefit of savings, but it’s also a weakness.

How It Usually Plays Out

Most people don’t intentionally drain their pet savings.

It happens gradually:

- You dip into it for something small

- You plan to replace it next month

- Something else comes up before you do

Over time, the balance doesn’t grow the way you expected. It builds, dips, rebuilds, and never quite gets ahead.

And that’s where the difference between saving money and having a true safety net becomes clear.

Why Saving Isn’t The Same As Having A True Safety Net

This is where a key distinction gets missed.

Saving money for your dog and being prepared for a major, unexpected expense aren’t the same thing.

They solve different problems.

What A Savings Fund Does Well

A savings account works like a sinking fund — it’s built for costs you can reasonably expect over time.

Things like:

- Routine vet visits

- Vaccines

- Professional dental cleanings

- Minor illnesses or medications (some pet insurance policies do cover prescription meds)

For these, saving works well. You’re spreading predictable expenses over time, and when they come up, the money is there.

Where It Starts To Struggle

The problem occurs when you try to use the same approach for large, unpredictable events, because such systems depend on one thing: Time.

And as you’ve already seen, major vet bills don’t always give you that time.

What A True Safety Net Does Differently

A real safety net isn’t something you slowly build toward. It’s something that’s already in place when something goes wrong.

The goal isn’t flexibility; it’s reliability.

Why This Distinction Matters

When people say, “I’ll just save instead,” they’re usually using a savings strategy to solve a safety net problem.

And sometimes that works if nothing major happens early. But when something does, that’s when the gap becomes obvious.

Because these two tools aren’t interchangeable:

- Savings handles the expected

- A safety net handles the unexpected

And once you separate those roles, the next step becomes a lot clearer.

Savings vs. Insurance (Quick Comparison)

Savings:

- Builds over time

- Flexible

- Works well for expected costs

- Can fall short early

Insurance:

- Active after waiting period

- Covers high, unexpected costs

- Predictable monthly cost

- Doesn’t cover pre-existing conditions

Most people don’t need to pick one—they need to understand what each actually does.

Why Pet Insurance Works From Day One

Up to this point, the pattern is clear: Saving takes time. Vet bills don’t.

That gap shows up most in the early months and years, when something serious happens before you’ve had time to build a meaningful balance.

This is where a different approach changes the equation, not by saving faster, but by removing the need to build up funds first.

How Pet Insurance Works Differently

With pet insurance, the structure is fundamentally different.

After a policy’s waiting period ends, you don’t have to build toward coverage — it’s already there.

So if something serious happens early, whether that’s a few months in or a year later, you’re not limited to what you’ve saved so far. You’re working with the coverage you chose.

Quick Note on Waiting Periods

All policies have short waiting periods before coverage begins once you purchase a policy. Accident coverage typically ranges from 0 to 15 days, while illness coverage is usually 14 days. Waiting periods may vary based on where you live.

Why That Changes Everything

Instead of trying to match a growing savings balance to a large, unpredictable expense, you’re shifting the problem entirely.

You’re trading a slow buildup of funds over time for immediate access to a much larger safety net.

That doesn’t replace budgeting or eliminate smaller costs, but it completely changes what happens in high-cost situations.

A simple way to think about it:

- Savings answers: “How much do I have right now?”

- Insurance answers: “What would I need if something serious happened today?”

That difference is what turns a plan that works eventually into one that’s usable right away.

The Moment A Vet Bill Becomes Real

There’s a moment when all of this stops being an idea. It’s when you’re sitting in a vet’s office or an emergency clinic, and you’re given a figure you weren’t expecting.

Not a range. Not a rough guess. A real estimate tied to a decision.

And in that moment, the question changes. It’s no longer: “Was saving $50 a month enough?” It becomes: “What can I do for my dog right now?”

That’s where having a true safety net changes everything.

It allows you to move forward with the care your dog needs immediately—instead of having to pause, delay, or start weighing less ideal options like financing or cutting back on treatment.

And once you look at it that way, the next question becomes pretty straightforward:

What does that kind of coverage actually cost, and is it worth it?

“But Isn’t Pet Insurance Expensive?”

This is usually the first question that comes up, and it’s a fair one.

Unlike a savings account, insurance is a recurring cost. You’re paying every month (or year) whether you use it or not, and over time, that adds up. There’s no getting around that.

What You’re Actually Paying For

It’s easy to view insurance as just another expense and compare it directly with savings.

But they’re not doing the same job.

- Savings = building toward a number over time

- Insurance = access to coverage you don’t have to build

You’re not just paying for reimbursement. You’re paying for the ability to handle a high, unexpected cost immediately, even if it happens early.

What Does Pet Insurance Actually Cost?

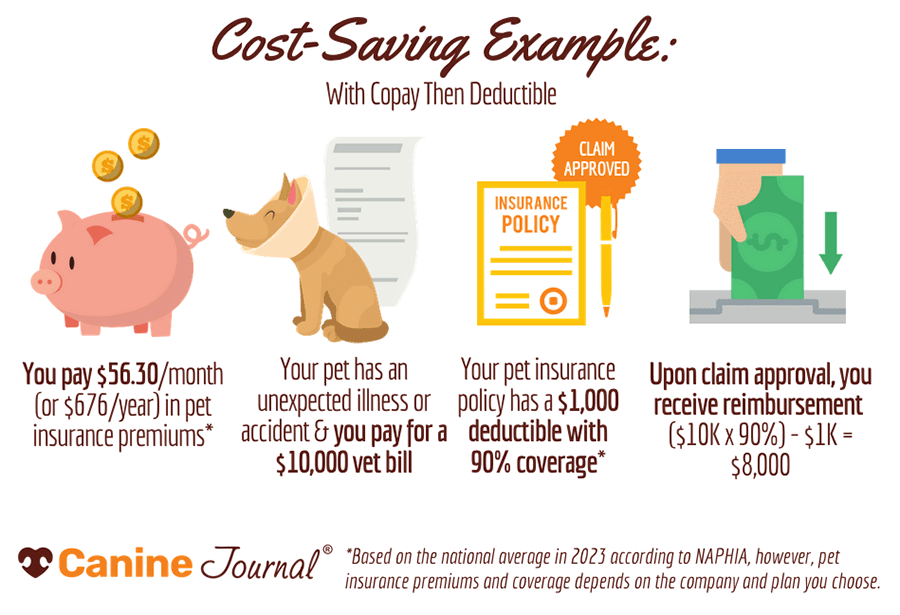

According to the NAPHIA (North American Pet Health Insurance Association), the average monthly premium for an accident and illness policy in the U.S. is:

- Dogs: $62.44/month

- Cats: $32.10/month

Actual costs vary based on your pet’s age, breed, location, and coverage level. But that’s the real-world range most people are working with.

A Different Way To Think About Cost

Instead of asking:

“Will I get my money’s worth?”

It can be more useful to ask:

“What would it cost me if something serious happened before I’m ready?”

Those are two very different questions. One focuses on long-term value. The other focuses on short-term risk.

Where This Lands For Most People

For some people, paying monthly for something they might never use doesn’t feel worth it.

For others, knowing they can say yes to treatment immediately feels like a better trade.

There’s no single right answer, but once you understand what each option is actually doing, the decision tends to get a lot clearer.

What Most Owners Regret (After the Fact)

Most people don’t regret saving money for their dog. They regret assuming they’d have enough when it actually mattered.

The hardest part isn’t the monthly cost or the planning; it’s the moment something happens, and you realize:

- The timing didn’t line up

- Your savings account isn’t where you thought it would be

- And the decision isn’t theoretical anymore

That’s when many owners wish they had set things up differently — not instead of saving, but alongside it.

Price Check Your Safety Net

At this point, the goal isn’t to make a big decision on the spot. It’s just to get a sense of what this would actually look like for you.

One of the biggest surprises for a lot of people is how much the cost can vary depending on your dog, your location, and the type of coverage you choose.

Why? Many top pet insurance providers give you a lot of flexibility to tailor your policy to fit your budget by choosing different levels of coverage (deductibles, reimbursement rates, etc.).

Instead of guessing, it’s worth taking a minute to check a few real quotes.

- See what monthly premiums look like

- Compare different coverage levels

- Get a feel for what fits your budget

It’s easy to dismiss something as “too expensive” when you don’t know the actual cost, but once you see real pricing, the decision becomes a lot more practical.

And it’s much easier to weigh that monthly number against:

- A $3,000 emergency

- A $5,000 surgery

- A situation where timing isn’t on your side

Quick Reality Check

If you strip everything down, here’s what it comes to:

- Saving grows slowly

- Vet bills don’t

- Most major costs aren’t predictable

- They tend to hit early and without warning

- Large expenses require immediate coverage

- Using savings for everything creates gaps

- Insurance works, but costs you upfront

The Hybrid Strategy: Do Both

For many people, the answer isn’t choosing one over the other. It’s using both in a way that actually matches how vet expenses show up.

In practice, that usually looks like this:

Savings handles the predictable:

- Routine vet visits

- Vaccines

- Minor illnesses

- Smaller out-of-pocket costs

Insurance handles the unpredictable:

- Emergencies

- Surgeries

- Major illnesses

- High-cost treatments

Each one is doing a different job, and that’s the point.

Frequently Asked Questions

Before we wrap up, here are a few of the most common questions people ask when trying to figure out whether saving, insurance, or a mix of both actually makes sense.

And if you’re still weighing your options, feel free to drop your question in the comments — there’s a good chance someone else is wondering the same thing.

Is $1,000 In Savings Enough For A Pet Emergency?

Short answer: sometimes, but often it’s not.

A $1,000 cushion can cover minor emergencies or diagnostics, but many serious issues, like surgeries or blockages, can quickly exceed that amount. It’s a helpful start, but not a complete safety net.

What’s The Most Expensive Vet Bill A Dog Can Have?

It depends, but some treatments can be surprisingly high.

- Emergency surgery: $3,000–$6,000+

- Orthopedic injuries (like CCL tears): $4,000–$6,500+

- Cancer treatment: $5,000–$10,000+

It only takes one major issue for costs to escalate quickly.

How Long Would It Realistically Take To Save Enough For A Major Surgery?

Longer than most people expect.

At $50/month, it takes about 8 years to reach $5,000. Even doubling that to $100/month still takes several years to fully cover the cost of a major procedure.

Can I Just Start Saving More Later If Something Happens?

Not in the moment that matters.

Vet bills typically require immediate payment or an on-the-spot decision. There’s no time to “catch up” on your savings when the expense is already in front of you.

What Happens If I Can’t Afford A Vet Bill?

This is the situation most people hope to avoid, but it does happen.

Options can include:

- Adjusting treatment plans

- Care Credit or other financing options

- Payment plans (if available)

But these decisions often come with tradeoffs, especially when timing is tight.

What If I Never End Up Using Pet Insurance?

That’s a common concern. In that case, you’ve essentially paid for access to coverage you didn’t need.

For some people, that tradeoff is worth it for the peace of mind. For others, it may not be.

It comes down to how you prefer to manage risk — paying a predictable monthly cost, or handling larger expenses if and when they happen.

Learn More About Pet Insurance

If you’ve made it this far, you already see where gaps can appear and why so many owners end up rethinking their plan after the fact.

The next step isn’t committing to anything. It’s just understanding what your options actually look like. Take a look at our expert guides:

A few minutes of research now can make a much bigger difference when timing isn’t on your side.

Have you ever had a vet bill hit before you were financially ready? What happened, and would you handle it differently now? Share your experience in our comments.